You're probably in one of two positions right now. You own a successful business in Brampton or Mississauga and you're tired of paying rent to someone else. Or you've built equity through residential real estate and you're starting to ask a sharper question: should the next move be a commercial real estate investment instead of another house or condo?

That's usually the turning point. A buyer notices a small plaza, an office unit, a warehouse bay, or a motel site and realises the rules are different, but the opportunity is bigger. Commercial property isn't just “residential, but larger.” It runs on leases, tenant covenants, operating costs, financing terms, zoning, and exit timing. If you understand those levers, you stop looking only at price and start looking at income, control, and future optionality.

In practical terms, that matters because commercial real estate sits inside a very large market. The U.S. commercial real estate investable universe was valued at $26.8 trillion as of H1 2024, and the sector generated an estimated $2.5 trillion in GDP in 2023, which helps explain why experienced investors treat it as a core wealth-building asset class, not a side play (Real Estate Roundtable CRE by the Numbers). In the GTA West, the same logic applies locally. The investors who do well aren't guessing. They match property type, financing, and neighbourhood-level demand to a clear business plan.

Table of Contents

- Beyond Your Home Unlocking Wealth with Commercial Real Estate

- Finding Your Fit An Investor's Guide to CRE Property Types

- Running the Numbers Key Metrics for Smart CRE Investments

- Structuring the Deal Commercial Financing and Tax Strategies

- Before You Sign The Essential Due Diligence Checklist

- Playing the Long Game Risk Management and Exit Strategies

- Investing in GTA West Your Next Steps with Team Arora Realty

Beyond Your Home Unlocking Wealth with Commercial Real Estate

A common first deal starts with an owner-operator. A business owner leases a unit for years, keeps improving the space, builds customer traffic, and then asks the obvious question: why am I paying down someone else's asset when I could own the building or buy into a property with income attached to it?

That question matters because commercial real estate investment changes how you build wealth. With residential property, the story is often appreciation first and monthly cash flow second. With commercial property, the conversation usually starts with the lease, the tenant, the operating expenses, and the income the building can produce from day one. That's a more disciplined framework, and for many buyers it's the first time real estate starts to feel like a business decision instead of a speculative one.

Why investors move beyond residential

Commercial assets can do three things that attract serious buyers:

- Create structured income: Leases are often more detailed than residential leases, with clearer rules around rent increases, maintenance, and tenant obligations.

- Build equity through operations: If you improve rents, reduce inefficiencies, or strengthen tenant quality, you may improve the value of the asset.

- Diversify your holdings: A plaza, office condo, industrial unit, or mixed-use property behaves differently from a detached home portfolio.

Practical rule: If you're buying commercial real estate only because it feels bigger, stop. Buy it because the income model is stronger and the business plan is clearer.

In GTA West, this becomes very tangible. A retail strip in Mississauga, a small industrial unit in Brampton, land in Halton Hills, or a hospitality asset near a highway corridor all require different underwriting. The opportunity isn't in owning “commercial” in general. It's in choosing the right asset for your capital, your time horizon, and your tolerance for operational complexity.

Finding Your Fit An Investor's Guide to CRE Property Types

Not every first commercial real estate investment should be a plaza or warehouse. The right property type depends on who will pay the rent, how long they'll stay, how much management the asset needs, and how exposed the property is to local demand shifts.

What each property type really buys you

Office works best for investors who understand tenant quality and leasing downtime. Professional offices can look stable on paper, but office leasing often requires negotiation around build-outs, inducements, and layout. In some locations, a medical or service-based office profile is easier to underwrite than a general office tenant because the use is more tied to place.

Retail is a street-level income play. You're not just buying square footage. You're buying visibility, parking, signage, access, and surrounding demographics. In GTA shopping corridors, retail investments in Brampton and Mississauga posted Q1 2025 average cap rates of 6.2%, and high foot traffic corridors can boost NOI by 18 to 22%, while triple-net structures yielded cash-on-cash returns of 7.5 to 9.2% for investors leveraging 65% LTV debt (GTA commercial retail investment data). That's why a mediocre plaza in the wrong node can underperform a smaller asset in the right trade area.

Industrial is usually the most straightforward commercial product to grasp. Think of it as operating infrastructure. Warehouses, flex units, and light industrial bays often have practical layouts, business tenants who value functionality over finishes, and uses tied to logistics, storage, fabrication, or last-mile distribution.

Commercial Real Estate Property Types at a Glance

| Property Type | Typical Lease Term | Tenant Profile | Management Intensity | Typical Risk/Reward |

|---|---|---|---|---|

| Office | Medium to long | Professional firms, medical users, service businesses | Moderate to high | Stable income if leased well, but leasing can be slow |

| Retail | Medium to long | Shops, restaurants, service operators, anchors | Moderate | Strong upside from location, but tenant quality matters a lot |

| Industrial | Medium to long | Logistics, trades, warehousing, light manufacturing | Lower to moderate | Often efficient to run, with demand tied to business activity |

| Multifamily | Shorter rolling tenancies | Households and renters | High | Defensive demand profile, but active management is required |

| Hospitality | Nightly or short-term occupancy | Travellers, crews, event traffic | High | Operational upside is significant, but it's management-heavy |

| Land | No lease unless interim use exists | Future developer, end user, or holding investor | Low now, high later | Highest patience requirement, with value tied to planning and timing |

Multifamily sits inside commercial financing and valuation logic once you move beyond smaller residential assets. Investors like it because housing demand tends to persist, but it is hands-on. Turnover, maintenance, collections, compliance, and management all matter every month.

Hospitality can be very profitable for the right operator and very punishing for the wrong one. A hotel or motel isn't just a building. It's an operating business wrapped inside real estate. Buyers need comfort with staffing, occupancy variability, and franchise or brand standards where applicable.

Land is the purest long game. You buy based on future use, servicing, access, entitlement prospects, and timing. That can create real upside, but there's no shortcut around planning risk.

The first commercial purchase doesn't need to be the biggest asset you can finance. It should be the one you can understand, hold through a rough patch, and improve with a clear plan.

For many first-time GTA West buyers, owner-occupied office, small-bay industrial, and necessity-based retail are easier entry points than pure development land or hospitality. Not because they're simple, but because the path from acquisition to stable income is usually easier to see.

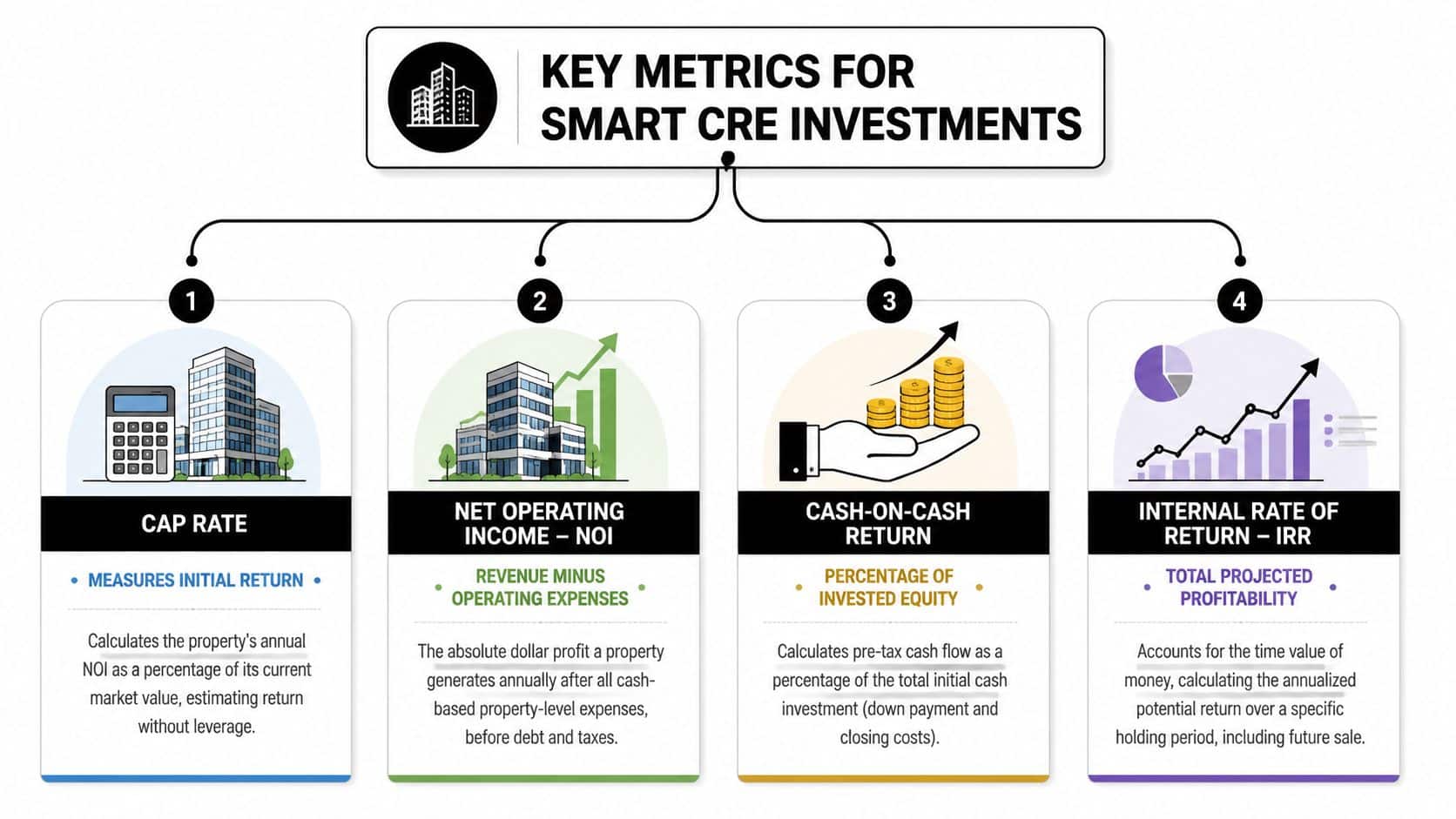

Running the Numbers Key Metrics for Smart CRE Investments

A commercial listing can look impressive and still be a poor investment. The cure is simple. Underwrite the income before you react to the building.

Four numbers that drive the decision

Net Operating Income, or NOI is the property's income after property-level operating expenses and before debt service and taxes. If a Brampton retail plaza collects rent and reimbursements, then pays for normal operating costs, what remains is the building's operating profit. NOI tells you whether the asset is productive. It's the number lenders, appraisers, and experienced buyers all focus on.

Cap rate is NOI divided by property value. The easiest way to explain it is unlevered yield. It helps you compare one property against another before financing enters the picture. A stronger cap rate isn't automatically better. Sometimes it signals more risk, weaker tenants, shorter lease terms, or a tougher location.

Cash-on-cash return asks a different question. What is your actual annual pre-tax cash flow compared with the cash you personally put into the deal? That matters because two properties with similar cap rates can produce very different investor outcomes once debt, closing costs, and reserves are included.

IRR, or internal rate of return, matters when the business plan has stages. It captures the timing of cash flows over a holding period, including income during ownership and value realised at sale. For value-add investors, IRR often matters more than a year-one yield because the upside may come later, after lease-up, renovations, or rezoning progress.

A practical underwriting workflow often starts with your rent roll, current expenses, and debt assumptions. For that financing layer, a tool that helps with integrated mortgage math for developers can be useful when you want to stress-test debt service, equity requirements, and different amortisation scenarios before you formalise an offer.

How the market changes your math

The market also changes how you interpret those metrics. Cap rates began increasing in 2022, forecasts indicated they would peak in 2024 before a steady decline, and the 2026 outlook points to increased capital availability with strong fundamentals across multifamily, industrial, and retail segments (commercial real estate cap rate outlook). That means investors need to separate temporary pricing dislocation from permanent asset weakness.

Here's the practical takeaway:

- Start with actual income: Ask for leases, amendments, and current operating statements.

- Normalise the expenses: Remove one-time anomalies and identify deferred costs.

- Model debt conservatively: Don't assume the lender sees the deal as generously as you do.

- Test the exit: A property only works if the next buyer will accept your future assumptions.

Buy based on verified income, not brochure language. If the seller says “upside,” your job is to decide whether that upside is probable, expensive, or imaginary.

Structuring the Deal Commercial Financing and Tax Strategies

Many residential investors underestimate this part. Commercial financing isn't just a larger mortgage. The lender is underwriting the property, the tenant income, the borrower, the use, and the exit risk all at once.

How commercial lending differs from residential

In residential lending, the borrower's income often carries the file. In commercial lending, the property's income matters far more. A lender wants to know whether the asset can support debt service, whether the tenant profile is stable, and whether the building remains marketable if something goes wrong.

That changes how buyers should think about the deal:

- The down payment is only one part of the equity story: Closing costs, legal fees, due diligence costs, lender fees, and reserves affect your true cash requirement.

- Lease quality affects financing terms: A strong tenant with a clean lease can improve lender comfort. Vacancy, short terms, or weak covenants usually do the opposite.

- Amortisation and loan term are separate decisions: A buyer can have manageable payments on paper and still face refinancing pressure when the term ends.

For owner-occupiers, the financing discussion also includes business stability. Lenders will often examine the business using the space, not just the building itself. For investors, the questions are sharper: who pays, for how long, and under what lease structure?

Where tax planning changes the outcome

Tax planning shouldn't start after closing. It should shape how you buy and how you hold title.

In Canadian commercial real estate, Capital Cost Allowance can be a powerful tool because it may allow an investor to deduct a portion of eligible building value over time, which can reduce taxable income from the property. The exact treatment depends on asset type, structure, allocation, and advice from your accountant and lawyer, but the principle is straightforward. The after-tax return on a deal can look meaningfully different from the pre-tax return.

A few practical habits help:

- Use the right ownership structure: Some buyers hold personally, others through a corporation or partnership.

- Allocate the purchase properly: Land and building are treated differently.

- Coordinate legal and accounting advice early: Fixing structure mistakes after closing is harder than planning well before the offer goes firm.

Commercial buyers who treat financing and tax as paperwork usually overpay in risk. Buyers who treat them as part of the investment strategy usually make cleaner decisions from the start.

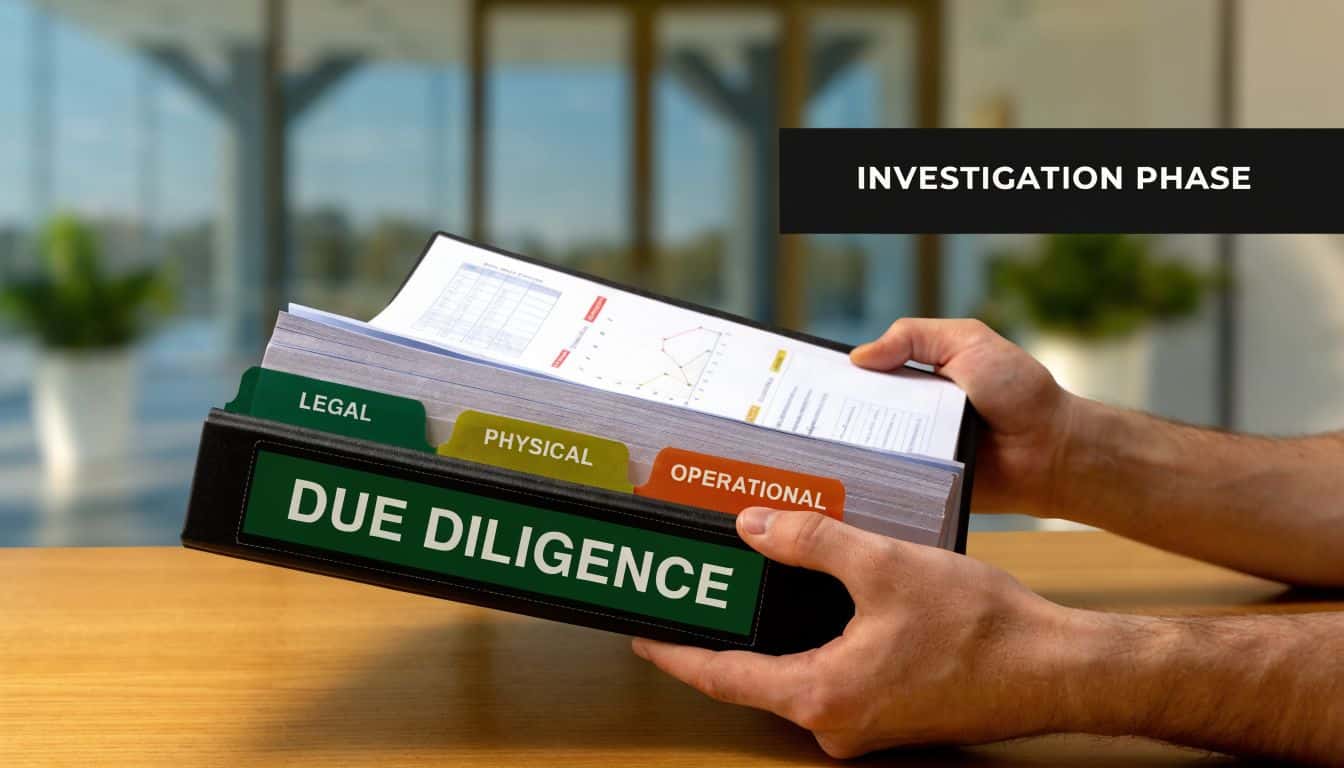

Before You Sign The Essential Due Diligence Checklist

The best commercial real estate investment deals usually survive scrutiny. The weak ones need optimism to stay alive.

A proper due diligence period is where you verify the income, inspect the building, confirm the legal use, and uncover the problems that never appear in the marketing package. New investors often focus too narrowly on the purchase price. Experienced investors focus on what could interrupt rent, delay financing, or create an unexpected capital requirement after closing.

Physical and operational checks

Start with the building itself. You need to know the condition of the roof, HVAC, electrical systems, plumbing, structure, paving, life-safety systems, and any specialised improvements. If the property has restaurant infrastructure, medical build-outs, or industrial power requirements, those elements need closer review because replacement or compliance costs can be significant.

Use a checklist that includes:

- Building inspection: Hire the right inspector for the asset type, not just a generalist.

- Environmental review: A Phase I Environmental Site Assessment is often essential, especially for industrial, automotive, older retail, and land sites.

- Deferred maintenance log: Ask what the seller postponed and what the tenants are already complaining about.

- Service contracts: Review waste removal, snow, HVAC maintenance, security, and any recurring vendor agreements.

Problems don't usually kill a deal by existing. They kill it when the buyer discovers them too late to renegotiate price, terms, or conditions.

This short walkthrough is worth watching before you finalise your process:

Legal and financial review

The paper side matters just as much as the bricks.

Read every lease, amendment, renewal option, notice provision, and tenant responsibility clause. Confirm who pays for repairs, taxes, insurance, and common area costs. Verify whether rents shown in the package match executed lease documents and actual deposits.

Then confirm legal use and title position:

- Zoning compliance: Verify the current use with the municipality. Don't assume a prior use is automatically permitted for your intended plan.

- Title and encumbrances: Review easements, rights-of-way, restrictions, liens, and any registrations affecting access or redevelopment.

- Operating statements: Match reported numbers against supporting records, not just seller summaries.

- Tenant estoppels where available: They can confirm rent, term, defaults, and side agreements.

If you're buying with a repositioning angle, due diligence also means checking whether the municipality is likely to support that use. On many GTA West files, the value isn't in the existing condition alone. It's in whether the site can legally become something better.

Playing the Long Game Risk Management and Exit Strategies

The investors who last in commercial real estate investment aren't the ones who avoid all risk. They're the ones who price it correctly, contain it, and give themselves more than one way out.

Threats that hurt first-time investors

Vacancy is the first threat. In Peel Region, commercial vacancy reached 8.2% for industrial and 12.5% for retail in Q1 2025, up 2.3% year over year, which is why loose assumptions around lease-up can be dangerous (GTA West risk and vacancy context). Buyers who underwrite immediate full occupancy often end up funding the gap themselves.

Interest rate pressure is the second threat. Even if rates stabilise, refinancing risk doesn't disappear. You need enough income resilience to carry the asset if credit is tighter when your term matures.

The third threat is operational leakage. Insurance gaps, weak lease enforcement, and poor maintenance control can erode returns. For investors with contractor-heavy tenants, trades uses, or improvement work underway, it helps to understand commercial property insurance for contractors because the risk profile can differ from a simpler office or retail tenancy.

One local mitigation strategy deserves attention. In Peel, investors are looking at mixed-use flex spaces near transit hubs such as Brampton Gateway Terminal, where data points to 15% year-over-year rent growth potential tied to rezoning entitlements in certain locations from the same GTA West market analysis above. That kind of defensive uplift can matter because it gives the buyer an income story today and a planning story tomorrow.

Plan the exit before the purchase

A first-time investor should be able to answer one question before removing conditions: how do I get my money back, and under what scenario?

Common exits include:

- Sell after stabilisation: Improve occupancy, clean up leases, and sell to a lower-risk buyer.

- Refinance and hold: Pull equity once the income improves and keep the asset for cash flow.

- Hold long-term: Best when the tenant profile is durable and the location supports future rent growth.

- Reposition for a higher use: Suitable only when zoning, market demand, and capital all support the change.

Buy with two exits in mind. If your primary plan fails, the backup should still protect your capital.

Investing in GTA West Your Next Steps with Team Arora Realty

A first commercial deal in GTA West usually gets decided by street-level details, not broad national theory. In Mississauga, two industrial pockets can price very differently based on truck access, power, and proximity to major routes. In Brampton, a flex unit often gets valued for functionality first. In Cambridge, older plazas and hospitality properties can make sense if the tenancy and traffic pattern are clear. In Halton Hills, land can work well, but only for buyers who understand servicing, zoning, and timing.

Where new investors are finding openings

New investors in this part of the market are often entering through smaller owner-user properties, co-ownership structures, or commercial assets that need leasing work and a tighter operating plan. That is common in GTA West because many buyers are balancing business growth, mortgage capacity, and a limited margin for error on their first purchase.

The practical question is not which listing looks best online. The practical question is which asset you can finance, operate, and hold through a slower leasing period or an unexpected repair.

That is where local brokerage advice matters. A buyer looking at a small retail plaza in Cambridge faces a different set of risks than a buyer considering an industrial condo in Mississauga or a parcel of future-use land in Halton Hills. Lease terms, permitted use, tenant quality, parking, and site constraints all affect value. So does the buyer's own plan. An owner-occupier needs different terms than a passive investor. A family co-purchase needs clearer documents and decision rules than a single-borrower acquisition.

For buyers who want a local starting point, Team Arora Realty commercial real estate services across GTA West provides brokerage, leasing support, land development guidance, and access to resale, exclusive, bank-owned, and some pre-construction opportunities across Brampton, Mississauga, Cambridge, Halton Hills, and the wider GTA. The benefit of working with a specialized brokerage is simple. Property search, underwriting support, local market context, and negotiation stay connected instead of getting handled in isolation.

What to do next

If you are serious about a first acquisition, keep the first moves disciplined:

- Decide your role early: investor, owner-occupier, or co-owner.

- Start with one asset class: retail, industrial condo, small office, mixed-use, or land. Do not chase all of them at once.

- Set the full capital plan: down payment, closing costs, lender requirements, immediate repairs, and reserves.

- Study the micro-location: demand on that corridor, competing supply, access, parking, and use restrictions matter as much as the building.

- Line up the deal team before you bid: broker, lender, lawyer, accountant, inspector, and if needed, a planner.

I tell first-time buyers the same thing in Brampton and Mississauga. The right first deal is usually not the flashiest property on the market. It is the one you can explain clearly on paper, carry with confidence, and improve with a realistic plan.

If you are weighing a purchase in Brampton, Mississauga, Cambridge, or Halton Hills, start with your budget, target property type, and timeline. Then screen opportunities against those limits before you get attached to a listing. That approach saves money, reduces bad assumptions, and usually leads to a better first commercial buy.

Crafted with Outrank