Canada Day is a time to celebrate home, community, family, and the future. Every July 1, Canadians come together for fireworks, local events, barbecues, road trips, and meaningful time with loved ones. It is also a perfect moment to think about what “home” really means and where your next chapter could begin.

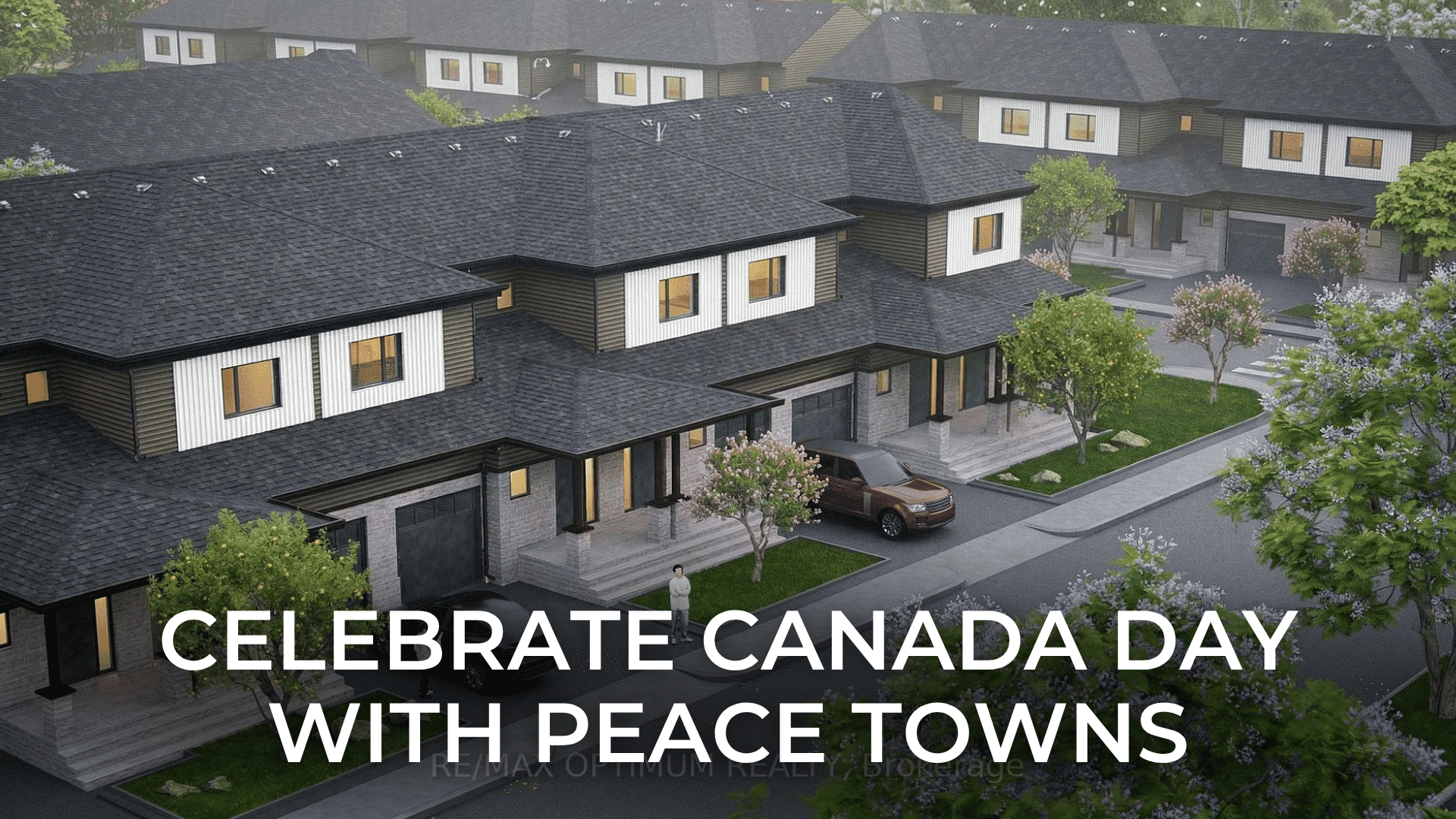

For buyers looking for a modern home in a growing Ontario community, Peace Towns in Fort Erie offers a timely opportunity. Located near Walden Boulevard and Garrison Road, Peace Towns brings together new townhome living, everyday convenience, and quick access to one of Canada’s most important border connections: the Peace Bridge.

According to the official Peace Towns website, the community features 36 luxury townhomes near the Peace Bridge and close to everyday conveniences such as Walmart, Canadian Tire, Sobeys, TD Bank, and Shoppers Drug Mart. For families, first-time buyers, downsizers, professionals, and investors, this is a community worth exploring this Canada Day season.

In celebration of Canada Day, Team Arora is also highlighting two new Peace Towns listing opportunities on Walden Boulevard. Both are modern 2-storey townhomes in Fort Erie, offering practical layouts, 3 bedrooms, 3 bathrooms, attached parking, and excellent future potential. Exact prices are not shown here, but interested buyers can contact Team Arora directly for current pricing, availability, floor plans, and offer details.

Table of Contents

- Why Canada Day Is the Perfect Time to Think About Home

- Peace Towns Fort Erie Community Overview

- Why the Fort Erie Location Matters

- Two New Peace Towns Listings Now Available

- New Listing 1: POTL Lot 14 Walden Boulevard

- New Listing 2: POTL Lot 17 Walden Boulevard

- Canada Day Lifestyle: Why Fort Erie Feels Like Home

- Why Buyers Are Looking at Peace Towns

- Investor and Long-Term Value Considerations

- How Team Arora Can Help

- Frequently Asked Questions

- Professional Disclaimer

- Sources and Citations

Why Canada Day Is the Perfect Time to Think About Home

Canada Day is more than a long weekend. It is a celebration of belonging, community, and the places we are proud to call home. Whether you are watching fireworks, spending time with family, visiting local parks, or planning a summer move, Canada Day naturally reminds us of the importance of stability and lifestyle.

For many buyers, the idea of home has changed. Today’s buyers want more than square footage. They want comfort, convenience, value, flexibility, and a community that supports their lifestyle. That is why new-home communities outside the GTA, such as Peace Towns in Fort Erie, are becoming more attractive.

Instead of only looking at major urban centres, buyers are exploring areas where they can enjoy more space, a quieter pace, everyday amenities, and strong long-term potential. Fort Erie offers that kind of lifestyle, especially for buyers who appreciate Niagara Region living and cross-border convenience.

Practical rule: Canada Day is a great time to reflect on where you live now, where you want to be next, and what kind of community truly fits your future.

Peace Towns Fort Erie Community Overview

Peace Towns is a new townhome community designed for buyers who want modern living in a convenient Fort Erie location. The project is located near Walden Boulevard and Garrison Road, placing residents close to daily shopping, services, and the Peace Bridge.

The official Peace Towns website highlights the community as a limited collection of 36 luxury townhomes. Buyers can register for priority updates, pricing details, early floor plan access, and exclusive offers.

The official floor plan page also describes 2,408 sq. ft. of thoughtfully designed living space across three levels, including the ground floor, first floor, and basement layout. Buyers should confirm final usable space, included finishes, upgrades, and purchase terms directly before making a decision.

Peace Towns Highlights

- Modern townhome community in Fort Erie

- Located near Walden Boulevard and Garrison Road

- 36 luxury townhomes, according to the official project website

- Minutes from the Peace Bridge

- Close to Walmart, Canadian Tire, Sobeys, TD Bank, and Shoppers Drug Mart

- Practical multi-level townhome layouts

- Appealing option for first-time buyers, families, downsizers, and investors

- New-home opportunity outside higher-priced GTA markets

Why the Fort Erie Location Matters

Fort Erie offers a unique lifestyle for buyers who want convenience, value, and access. Peace Towns is positioned close to Garrison Road, one of the area’s important corridors for shopping, services, and daily errands.

The location also gives residents access to the Peace Bridge, which connects Fort Erie, Ontario, with Buffalo, New York. For buyers with family, business, travel, or lifestyle connections across the border, this can be a meaningful advantage.

Fort Erie also offers access to local parks, trails, waterfront areas, beaches, shopping, and community events. During Canada Day, the area becomes even more special as residents enjoy local celebrations, family gatherings, and fireworks across the Niagara Region.

Location Benefits Near Peace Towns

- Close to the Peace Bridge and Canada-U.S. border connection

- Near Garrison Road shopping and everyday services

- Convenient access to groceries, pharmacy, banking, and retail

- Located within the broader Niagara Region lifestyle market

- Appealing for buyers looking outside the GTA

- Useful for families, professionals, retirees, and investors

Two New Peace Towns Listings Now Available

This Canada Day season, Team Arora is highlighting two new listing opportunities within the Peace Towns community. Both listings are located on Walden Boulevard in Fort Erie and offer modern townhome living in a growing area.

Exact prices are not shown in this blog, but buyers can contact Team Arora directly for the latest pricing, current availability, floor plans, deposit information, incentives, and next steps.

Interested buyers should act early, because limited new-home communities can move quickly when pricing, location, and layout align with buyer demand.

New Listing 1: POTL Lot 14 Walden Boulevard

The first featured opportunity is POTL Lot 14 Walden Boulevard in Fort Erie. This listing is part of the Peace Towns community and is identified under MLS® number X13498282.

This beautifully designed 2-storey corner lot townhome offers a bright and functional layout with modern everyday comfort. Public listing details describe the home as offering 3 bedrooms, 3 bathrooms, approximately 1,500 to 2,000 sq. ft. of living area range, 2 parking spaces, central air conditioning, forced-air natural gas heating, and a full unfinished basement.

The open-concept main floor is designed for comfortable living, with space for family time, entertaining, and everyday routines. The unfinished basement adds future potential, giving buyers flexibility for storage, recreation, fitness space, a home office, or future finishing, subject to approvals and buyer needs.

Highlights of POTL Lot 14 Walden Boulevard

- Peace Towns community opportunity

- 2-storey corner lot townhome

- 3 bedrooms

- 3 bathrooms

- Approx. 1,500 to 2,000 sq. ft. living area range

- 2 parking spaces

- Central air conditioning

- Forced-air natural gas heating

- Full unfinished basement with future potential

- Suitable for families, first-time buyers, or investors

Pricing note: Exact price is intentionally not displayed in this blog. Please contact Team Arora for current pricing and availability.

New Listing 2: POTL Lot 17 Walden Boulevard

The second featured opportunity is POTL Lot 17 Walden Boulevard in Fort Erie. This listing is identified under MLS® number X13498290 and is also part of the Peace Towns community.

Public listing details describe this property as a 2-storey attached/row/townhouse with 3 bedrooms, 3 bathrooms, 2 parking spaces, and approximately 1,500 to 2,000 sq. ft. of living area range. It is positioned in the Lakeshore community of Fort Erie, near Garrison Road and Concession Road.

The home offers a practical modern layout with an open-concept main floor, a spacious great room, a modern kitchen, and comfortable living space. Upstairs, buyers can expect three bedrooms, including a primary bedroom with ensuite access, along with additional bathroom convenience for the household.

Premium features referenced in public listing details include stainless steel appliances, fridge, stove, hood range, dishwasher, washer and dryer, central air conditioning, forced-air gas heating, municipal water and sewer, attached single-car garage, private driveway, brick veneer and vinyl siding exterior, asphalt shingle roof, and a full unfinished basement.

Highlights of POTL Lot 17 Walden Boulevard

- Peace Towns community opportunity

- 2-storey attached/row/townhouse

- 3 bedrooms

- 3 bathrooms

- Approx. 1,500 to 2,000 sq. ft. living area range

- 2 parking spaces

- Modern open-concept main floor

- Stainless steel appliance package referenced in public listing details

- Attached garage and private driveway

- Full unfinished basement with future potential

- Close to QEW, Peace Bridge, shopping, schools, parks, and everyday amenities

Pricing note: Exact price is intentionally not displayed in this blog. Please contact Team Arora for current pricing and availability.

Canada Day Lifestyle: Why Fort Erie Feels Like Home

Canada Day is the perfect time to imagine life in a community like Fort Erie. The day often brings together everything buyers value in a neighbourhood: family time, outdoor spaces, local pride, community events, and a strong sense of belonging.

Fort Erie offers access to waterfront destinations, local parks, recreational trails, shopping, restaurants, and the Peace Bridge. For buyers moving from larger markets, this can feel like a refreshing lifestyle change. Peace Towns adds to that lifestyle by offering modern townhome living close to daily conveniences.

Why Canada Day connects naturally with Peace Towns

- Canada Day celebrates home, community, and belonging.

- Peace Towns offers a new-home opportunity in a growing Ontario community.

- Fort Erie offers a relaxed lifestyle with access to Niagara Region amenities.

- The Peace Bridge location adds a unique Canada-U.S. connection.

- New listings give buyers a timely opportunity to explore the community.

Why Buyers Are Looking at Peace Towns

Peace Towns appeals to buyers who want a balance of modern design, practical space, and location value. Many buyers are looking beyond the GTA for more attainable ownership opportunities, and Fort Erie is becoming part of that conversation.

For first-time buyers, Peace Towns may offer a chance to enter the market with a new townhome. For families, the 3-bedroom layouts and future basement potential are practical. For downsizers, the community offers new construction and everyday convenience. For investors, the location near Garrison Road, the Peace Bridge, and Niagara Region amenities may support long-term interest.

Buyer Benefits

- Modern 2-storey townhome living

- 3-bedroom layouts suitable for families and professionals

- Close to shopping, schools, parks, and services

- Peace Bridge and QEW access

- Attached parking and practical layouts

- Full unfinished basement potential

- New-home community appeal

- Attractive option for buyers looking beyond the GTA

Investor and Long-Term Value Considerations

For investors, Peace Towns may be worth reviewing because of its location, new-build appeal, and Fort Erie’s growing interest among buyers looking for value outside major urban markets. However, investors should always review the numbers carefully before making a decision.

Rental demand, carrying costs, property taxes, insurance, maintenance, financing, vacancy risk, resale comparables, and future growth plans should all be considered. A strong location story is helpful, but investment decisions should always be based on verified information and professional advice.

Investors should review:

- Current pricing and purchase terms

- Deposit structure

- Mortgage qualification and monthly payments

- Estimated rent in Fort Erie

- Vacancy risk

- Property taxes and insurance

- Future resale comparables

- Maintenance and repair responsibilities

- Closing costs and adjustments

- Long-term growth in the surrounding area

Practical rule: A good investment is not only about buying at the right price. It is about understanding cash flow, demand, expenses, risk, and exit strategy.

How Team Arora Can Help

Team Arora can help buyers explore Peace Towns and understand which opportunity best fits their goals. Whether you are a first-time buyer, family, downsizer, or investor, the right guidance can make the process easier and more informed.

With two new Walden Boulevard listings available, buyers can speak with Team Arora to review current pricing, availability, floor plans, features, closing timelines, mortgage options, and next steps.

Team Arora can help with:

- Peace Towns project information

- Current pricing and availability

- Lot 14 and Lot 17 listing details

- Floor plan comparison

- Feature and upgrade review

- Mortgage and affordability planning

- Fort Erie market guidance

- Investment and resale considerations

- Offer strategy and purchase guidance

If you are ready to explore Peace Towns this Canada Day season, contact Team Arora for details on the two new listings and available buying opportunities.

Frequently Asked Questions

What is Peace Towns in Fort Erie?

Peace Towns is a new townhome community near Walden Boulevard and Garrison Road in Fort Erie. The official project website describes it as a 36-townhome community minutes from the Peace Bridge and close to everyday conveniences.

Where is Peace Towns located?

Peace Towns is located near Walden Boulevard and Garrison Road in Fort Erie, Ontario. The area offers access to shopping, services, the Peace Bridge, and the broader Niagara Region lifestyle.

What are the two new Peace Towns listings?

The two featured listings are POTL Lot 14 Walden Boulevard, MLS® X13498282, and POTL Lot 17 Walden Boulevard, MLS® X13498290. Both are modern 2-storey townhome opportunities in Fort Erie.

Are the exact prices shown in this blog?

No. Exact prices are intentionally not shown in this blog. Buyers should contact Team Arora directly for the latest pricing, current availability, and offer details.

How many bedrooms and bathrooms do the featured listings have?

Both featured opportunities are described in public listing details as offering 3 bedrooms and 3 bathrooms. Buyers should verify all current listing information directly before making a decision.

Is Peace Towns good for first-time buyers?

Peace Towns may appeal to first-time buyers who want a modern townhome outside higher-priced GTA markets. Buyers should review mortgage approval, monthly payments, closing costs, and long-term affordability before purchasing.

Is Peace Towns good for investors?

Peace Towns may appeal to investors because of its new-home format, location near Garrison Road, Peace Bridge access, and Fort Erie growth potential. Investors should review rental demand, carrying costs, financing, and resale comparables before buying.

How can I get current pricing?

Contact Team Arora directly to request current pricing, available lots, floor plans, incentives, and next steps for Peace Towns.

Professional Disclaimer

This article is provided for general informational and real estate marketing purposes only. It should not be treated as legal, financial, mortgage, tax, investment, appraisal, construction, warranty, or real estate advice. Listing details, availability, pricing, square footage, features, finishes, taxes, incentives, closing dates, and purchase terms can change without notice.

Exact listing prices are intentionally not displayed in this blog. Buyers should contact Team Arora or the listing representative directly to confirm current pricing, availability, MLS details, offer terms, and all property information before making a decision.

All buyers should verify current project and listing details directly with the developer, builder, sales representative, brokerage, municipality, lender, insurer, home inspector, and lawyer before purchasing. Any investment discussion is general in nature and does not guarantee rental income, resale value, appreciation, occupancy timing, or financial return.

Sources and Citations

Government of Canada — Canada Day

— Canada Day celebrations, July 1 events, ceremonies, shows, fireworks, and national holiday information.

Peace Towns — Official Project Website

— Project overview, 36 luxury townhomes, location near Walden Boulevard and Garrison Road, Peace Bridge proximity, amenities, and registration information.

Peace Towns — Official Floor Plans

— Advertised 2,408 sq. ft. of living space across three levels, including ground floor, first floor, and basement layout details.- MLS® X13498282 — POTL Lot 14 Walden Boulevard, Fort Erie

— Listing details reviewed for property type, bedroom count, bathroom count, parking, living area range, heating, cooling, basement, and community information. - MLS® X13498290 — POTL Lot 17 Walden Boulevard, Fort Erie

— Listing details reviewed for property type, bedroom count, bathroom count, parking, living area range, layout, appliances, garage, driveway, basement, and location details.

This Canada Day, celebrate more than the holiday. Celebrate the possibility of a fresh start. Peace Towns in Fort Erie offers modern townhome living, everyday convenience, and a location connected to both Niagara Region and the Peace Bridge. With two new Walden Boulevard opportunities now available, this may be the right time to explore what Peace Towns can offer.

Contact Team Arora today for current pricing, availability, floor plans, and private guidance on POTL Lot 14 and POTL Lot 17, Walden Boulevard.