You're usually not reading about how to sell a house fast for fun. There's a move coming. Maybe you already bought. Maybe you're relocating, separating households, handling an estate, or trying to stop one property from draining cash every month it sits unsold.

In Brampton, Mississauga, Cambridge, and Halton Hills, fast sales don't happen because a seller “gets lucky”. They happen because the listing is positioned correctly from day one. Price, presentation, launch timing, showing control, and offer strategy all have to line up. Miss one piece and the home can stall. Once that happens, buyers start negotiating from your weakness instead of your strength.

The good news is that speed and strong pricing aren't opposites. They often support each other when the home is prepared properly and launched with discipline.

Table of Contents

- Strategic Pricing for a Quick Sale in the GTA

- Rapid Repairs and Staging for Maximum Impact

- Aggressive Marketing to Attract Ready Buyers Now

- Managing Showings and Offers for a Swift Agreement

- Exploring Fast-Track Sale Options Beyond the MLS

- Your Closing Checklist for a Smooth Handover

Strategic Pricing for a Quick Sale in the GTA

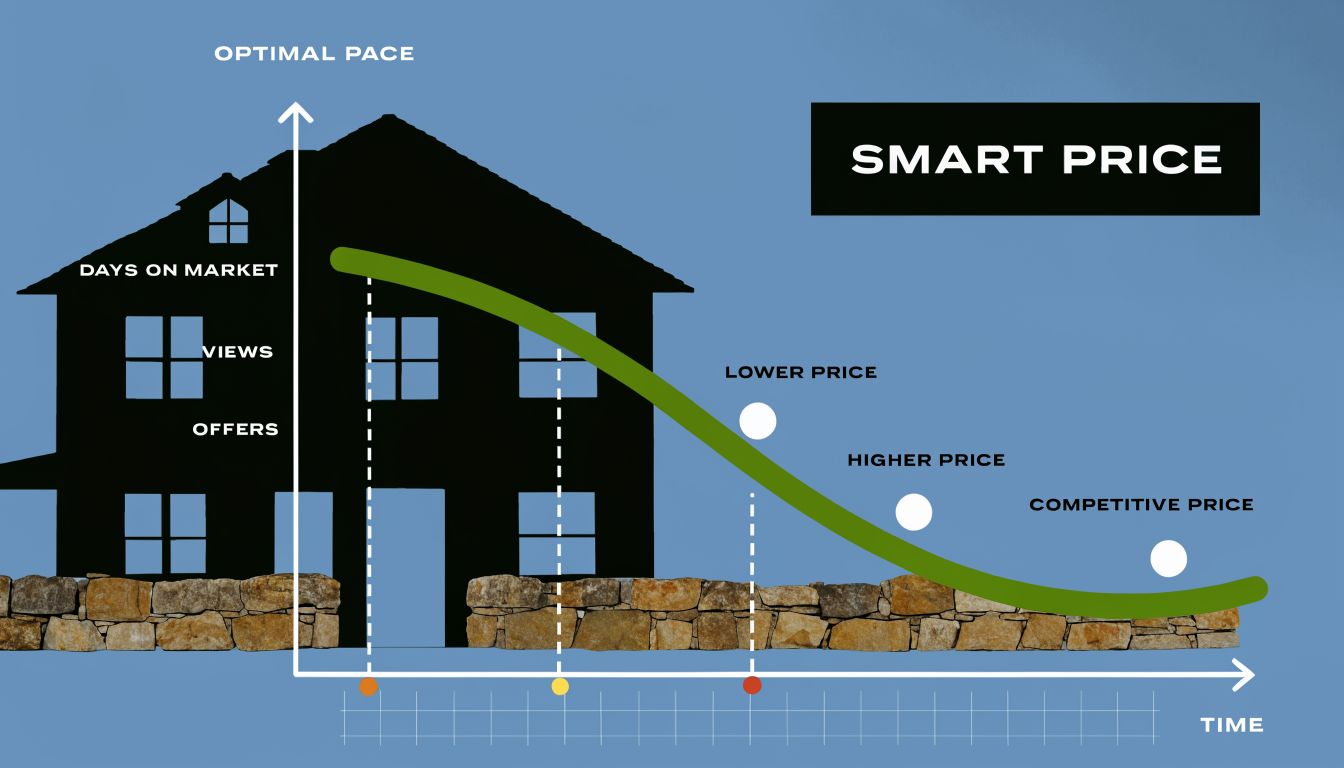

If you want speed, pricing is the first real decision. Not photography. Not staging. Not ad spend.

Most sellers are balancing two goals that pull against each other. One is extracting every possible dollar. The other is creating enough urgency that buyers act quickly and compete. In a shifting market, especially across different GTA submarkets, trying to “leave room to negotiate” often backfires. An overpriced listing doesn't create an upper hand. It creates hesitation.

Start with the speed versus price trade-off

A fast sale usually comes from pricing close to where buyers already agree the home belongs. In Brampton and Mississauga, that means watching not just active competition, but what similar homes have sold for very recently. In Cambridge and Halton Hills, it also means accounting for how buyer pools change by property type, lot style, and commute appeal.

Use this sequence:

- Pull recent sold comparables first. Ignore the temptation to anchor to hopeful active listings.

- Segment by micro-market. A detached home in one pocket of Mississauga won't behave like a similar home a few postal codes away.

- Read the speed signals. If recent competing homes needed price cuts, buyers are pushing back.

- Choose your lane early. You can price for immediate attention or test the ceiling. You usually can't do both.

Practical rule: If your first wave of buyer attention is weak, the issue is usually price, positioning, or condition. It's rarely “marketing hasn't kicked in yet”.

Use psychological pricing properly

There is one pricing tactic that's simple and often worth using. According to HomeLight's summary of Zillow and Trulia pricing research, homes priced ending in .99 sold up to one week faster, and 53% of listings use a 9-ending price. In practice, a price like $799,900 often feels more natural to buyers than a rounder number above it.

This works even better when it helps you sit just under a key online search threshold. Buyers searching by cap price won't see a listing that falls outside their filter. A small pricing adjustment can expand your visible audience immediately.

What this looks like in Brampton, Mississauga, Cambridge, and Halton Hills

The mistake sellers make is treating the entire region as one market. It isn't.

- Brampton: Buyers compare quickly, especially in high-turnover neighbourhoods. Sharp pricing gets immediate traction.

- Mississauga: Presentation matters more because buyers often cross-shop lifestyle, commute, and school-zone options.

- Cambridge: Value perception is critical. Buyers tend to notice when a home is priced ahead of what nearby product is supporting.

- Halton Hills: Unique lots and less uniform inventory can make overpricing easier to justify emotionally and harder to defend once buyers compare.

A good agent should show you the local sale pattern and the current competition, then explain where your home fits. That's part of what firms such as Team Arora Realty build into a listing strategy for sellers who need a practical market analysis, prep plan, and launch structure.

For a useful outside perspective on fast-sale thinking in another market, this guide on selling Miami homes quickly for cash is worth reading. The geography is different, but the trade-off logic is the same. Speed comes from choosing the right path early, not improvising after the listing goes stale.

Rapid Repairs and Staging for Maximum Impact

Fast-selling homes don't need a full renovation. They need fewer objections.

Most buyers decide how they feel about a house before they analyse it carefully. If the home feels clean, bright, current, and easy to move into, they forgive minor imperfections. If it feels tired, cluttered, or unfinished, they start subtracting value in their heads.

The weekend shortlist that actually matters

If time is tight, focus on three things that buyers notice instantly:

- Lighting: Replace burnt bulbs, mismatched colour temperatures, and dated fixtures that drag the room backward.

- Paint: Patch obvious dings and repaint the loudest rooms in soft neutrals that make the home feel bigger and calmer.

- Curb appeal: Clean the entry, trim overgrowth, and make the front door area look maintained.

You don't need to make the house look expensive. You need to make it look organised and easy.

A lot of staging advice is too broad to be useful. If you want a grounded overview of buyer psychology and layout decisions, the art of preparing a home is a worthwhile read because it focuses on how rooms should feel, not just how they should look in photos.

Fix these before you spend on anything decorative

Cosmetic styling won't save a house with visible maintenance issues. Handle the problems that make buyers think, “What else is wrong here?”

- Leaky taps or running toilets: Small issue, big signal.

- Loose handles or sticking doors: Buyers remember friction.

- Cracked caulking: Especially in kitchens and baths.

- Scuffed walls at eye level: These make a home feel more worn than it is.

- Broken switches or dead fixtures: Every non-working item invites suspicion.

Buyers don't separate “small repairs” from “overall maintenance” the way sellers do. They see a pattern.

Power staging instead of full staging

A rushed sale benefits from restraint. Overfurnished rooms look smaller. Empty rooms can feel cold and harder to read. The sweet spot is what I'd call power staging. Enough furniture to define each room clearly, but not so much that the layout feels cramped.

Use these choices:

| Area | Keep | Remove |

|---|---|---|

| Living room | One main seating arrangement | Extra chairs, bulky side units |

| Bedrooms | Properly made bed, minimal tables | Personal collections, oversized dressers |

| Kitchen | One or two clean focal points | Countertop appliances, paper clutter |

| Entry | Clean mat, simple console if space allows | Shoe piles, seasonal overflow |

Video can help sellers understand how quickly visual changes affect a room's feel:

The room-by-room standard

In Brampton and Mississauga, family buyers often focus on function first. In Cambridge and Halton Hills, they also pay close attention to whether the home feels settled and move-in ready. Across all four markets, the standard is the same.

Each room should answer one question clearly: What is this space for?

If a dining room has become storage, convert it back. If a basement corner could be a work area, show it. If a spare bedroom is full of mixed-use furniture, simplify it. Fast sales come from fast comprehension. Buyers move quicker when the layout makes sense in seconds.

Aggressive Marketing to Attract Ready Buyers Now

A quick sale needs more than exposure. It needs a launch that concentrates attention.

When a listing drips into the market without momentum, buyers treat it casually. When the launch is timed and packaged properly, the home feels active from the start. That changes how agents book showings, how buyers prioritise viewings, and how quickly offers form.

Why Thursday is the strongest launch day

Timing matters. According to Zillow's best time to sell research, homes listed on a Thursday tend to go under contract faster than homes listed on other days. The logic is straightforward. Buyers and agents get enough time to review the listing and schedule weekend showings while the property still feels brand new.

In the GTA, that matters even more because weekend traffic is still where many serious buyers make decisions. A Thursday launch lets you stack interest instead of spreading it thin.

The listing package buyers expect now

Phone photos and a rushed description don't hold up anymore. If your goal is speed, the listing has to answer objections before a buyer ever books a showing.

The essential elements are:

- Professional photography: Bright, level, consistent images that make the home feel coherent.

- 3D virtual tour: Useful for filtering out casual shoppers and helping serious buyers commit to seeing it.

- Floor plans: Buyers want dimensions and flow, not just pretty corners.

- Compelling remarks: Not fluffy copy. Clear value, upgrades, layout benefits, and lot or location details.

A listing should make a buyer feel they already understand the property before they arrive. That reduces wasted showings and improves the quality of the ones you get.

Digital reach should be targeted, not noisy

Social promotion helps most when it's specific. Broad ads can create vanity traffic, but that doesn't sell homes. What works better is targeting likely buyer profiles by geography, housing intent, and lifestyle fit.

For example:

- A family home in Brampton should be marketed differently from a commuter-focused condo alternative in Mississauga.

- A property in Cambridge may need messaging that highlights value and usable space.

- A Halton Hills home often benefits from lifestyle framing, lot features, and privacy cues.

Serious marketing creates pre-qualified curiosity. It doesn't just chase clicks.

What good marketing does in the first few days

A strong launch does three things at once:

- It tells buyers this listing is fresh.

- It tells agents the seller is organised.

- It makes hesitant buyers worry they'll miss the opportunity.

That last point matters. Urgency doesn't come from hype. It comes from visible activity, easy scheduling, polished presentation, and a clear sense that the home won't sit around waiting for someone to think about it later.

If the first weekend lands properly, the rest of the sale becomes much easier. If it doesn't, you're usually trying to rebuild momentum instead of using it.

Managing Showings and Offers for a Swift Agreement

The launch gets attention. The showing and offer process turns that attention into a signed deal.

Too many sellers stay loose here. They allow scattered showings, vague offer expectations, and slow responses. That feels flexible, but it usually weakens your negotiating position. Buyers move faster when the seller's process is clear.

Control the showing flow

If the home is getting interest, don't spread showings randomly across too many days unless the market clearly calls for it. Tight showing windows can create healthy pressure. Buyers notice activity. Agents compare notes. A home that feels busy often gets treated as desirable.

That doesn't mean making access difficult. It means making access structured.

A practical setup often includes:

- Defined showing blocks: Concentrate traffic into periods when the home looks its best.

- Consistent prep standard: The house should show the same way every time.

- Immediate feedback collection: Don't wait days to learn what buyers are objecting to.

Offer day can work, but only when the setup supports it

An offer date is useful when the home is priced and marketed to attract enough attention early. In that scenario, holding offers can create a stronger environment because buyers know they're competing not just on price, but on terms.

If interest is moderate rather than intense, the same strategy can misfire. Buyers may hold back, assume the seller is unrealistic, or wait for the offer date to fail before circling back lower.

Use the approach that matches the response you're getting, not the one you hoped for before launch.

Strong sellers don't just ask, “What's the highest offer?” They ask, “Which buyer is most likely to close on time without drama?”

Evaluate the offer, not just the number

A fast sale is only fast if it becomes firm and closes smoothly. The headline price matters, but so do the terms behind it.

Review these points carefully:

| Offer element | Why it matters for speed |

|---|---|

| Financing condition | A weaker financing setup creates more uncertainty |

| Deposit strength | A serious buyer usually backs the deal decisively |

| Closing date | The right date can save stress and carrying risk |

| Inspection terms | Broad conditions can reopen negotiation later |

| Flexibility on inclusions | Smaller disputes can slow legal prep |

The strongest offer is often the one that combines acceptable price with fewer ways to collapse.

Keep negotiations tight and calm

Delays hurt momentum. When buyers don't hear back promptly, they start looking elsewhere or lose conviction. Respond quickly, even if the answer is a counter.

In competitive situations, stay consistent. Give all buyers the same instructions and deadlines. Avoid side conversations that create confusion or unfairness. If a bully offer appears before an offer date, assess it against the current activity objectively. Sometimes taking certainty early is smart. Sometimes it leaves money on the table. The right answer depends on buyer depth, not ego.

A clean process feels less emotional for everyone involved. That usually leads to better terms and fewer surprises after acceptance.

Exploring Fast-Track Sale Options Beyond the MLS

Not every seller should use the traditional listing route. Some need speed with certainty. Others need convenience more than maximum exposure. If that's your situation, you need to compare options by net outcome, not just headline price.

The central question is simple. What are you really buying when you choose a faster path? Usually it's some combination of time, convenience, repair avoidance, and reduced fallout risk.

Side-by-side comparison of the main paths

| Sale path | Best fit | Main advantage | Main trade-off |

|---|---|---|---|

| Traditional MLS sale | Sellers who can prepare and market properly | Widest buyer reach | More prep, showings, and variable timeline |

| Cash buyer program | Sellers prioritising certainty or selling as-is | Quick closing, fewer conditions | Offer may be lower |

| Broker network sale | Sellers with privacy concerns or niche buyer appeal | Controlled exposure | Smaller buyer pool |

| Pre-foreclosure sale | Sellers facing urgent timeline pressure | Preserves options before a more severe outcome | Less room to wait for ideal terms |

When a cash offer deserves serious consideration

Cash isn't automatically better. It's better when certainty has real value to you.

According to HomeLight's guidance on difficult-sale scenarios, deciding whether a guaranteed cash offer makes sense requires weighing a potentially lower headline price against savings on carrying costs, repair expenses, and the risk of a deal falling through on financing, especially in Ontario's changing rate environment.

That's the right framework. Compare the whole picture:

- Repairs you won't have to do

- Time you won't spend preparing the home

- Mortgage, tax, insurance, and utility carrying period

- Chance of a conditional buyer failing to close

- Stress cost if you're dealing with relocation, estate work, or tenant issues

For some sellers, that trade is worth it. For others, it's expensive convenience.

How this plays out in local markets

The right option can vary by municipality.

In Brampton, a move-in-ready family home often deserves MLS exposure because the buyer pool can be broad when the home is priced correctly. In Mississauga, presentation-heavy properties may benefit from full-market exposure because lifestyle marketing can materially affect demand. In Cambridge, homes needing work may attract investors or cash-style buyers more quickly if the seller doesn't want to renovate. In Halton Hills, off-market or selective-network approaches can sometimes make sense for unique homes where buyer targeting matters more than mass traffic.

A decision filter that keeps you honest

Ask yourself these four questions:

- How fast do you need to be sold? Immediate urgency changes the answer.

- What condition is the home in right now? If prep is extensive, speed alternatives become more attractive.

- How much uncertainty can you tolerate? Some sellers care more about firm terms than chasing the highest possible number.

- What is your real net, after time and costs? That's the number that matters.

Convenience has a price. Uncertainty has a price too. Smart sellers compare both.

iBuyers and hybrid fast-sale models

In Canada, iBuyer-style options exist less uniformly than in some U.S. markets, and they're not always the right fit for every property type or area. Still, the logic is similar. These programs appeal to sellers who want a simplified process and less market exposure.

The key is to read every adjustment carefully. A nominal offer can look strong until inspection adjustments, service charges, or convenience-related deductions appear. Always compare any direct-buy option against what a realistic MLS strategy could produce after prep costs and carrying time, not against your ideal number.

Your Closing Checklist for a Smooth Handover

Accepted doesn't mean finished. A lot of “fast” deals slow down in the closing period because sellers get disorganised after the hard part seems done.

The final stretch is administrative, legal, and logistical. Handle it early and the handover stays clean. Leave it late and small issues start pushing against the closing date.

Keep your documents ready

Your lawyer will need information quickly. Don't wait until the last week to gather it.

Have these organised:

- Property tax information

- Utility account details

- Survey or title-related documents if available

- Records for major inclusions that stay with the home

- Condominium documents if the property is a condo or townhome with management requirements

If anything is missing, tell your lawyer early. Silence creates delay.

Fulfil the deal exactly as signed

Sellers get into trouble when they treat accepted terms casually. If the agreement says an item is included, it should remain. If the contract requires vacant possession, the property needs to be empty on time. If a repair or condition has to be satisfied before closing, track it properly.

This is also where the earlier pricing discipline matters. As noted in Zillow's home-selling guidance, anchoring your price to current local sale-to-list trends and months of inventory for your municipality helps avoid the kind of overpricing that leads to reductions and slows the whole process. A clean closing often starts with a clean strategy long before lawyers are involved.

Use a simple final-week checklist

A straightforward handover plan prevents avoidable friction:

- Confirm moving dates early: Don't create overlap confusion with buyers, movers, or cleaners.

- Leave the property in the agreed condition: Broom-clean is the minimum. Better is cleaner than expected.

- Test included items: Appliances, remotes, garage access, and fixtures should still work.

- Set aside keys and access devices: Label everything clearly.

- Prepare for the buyer walkthrough: The home should look substantially the same as when it sold.

The smoothest closings happen when nothing feels like a surprise in the final forty-eight hours.

Think like the buyer's lawyer for one day

This helps more than most sellers realise. Ask what would trigger a last-minute call or complaint.

Was an included light fixture swapped out? Is there leftover junk in the shed? Are patch jobs obvious after wall-mounted TVs came down? Has the property been damaged during move-out? These details are small until they affect trust. Then they become large very quickly.

The handover should feel orderly. Buyers remember that. More importantly, orderly closings are far less likely to become stressful closings.

If you need to sell quickly in Brampton, Mississauga, Cambridge, or Halton Hills, Team Arora Realty can help you compare the right path for your timeline, whether that means a fully marketed MLS launch or a faster as-is alternative. The most effective plan starts with your actual constraints, your local market, and the net result you want at closing.

Drafted with Outrank tool