The Greater Toronto Area (GTA) condo market has entered 2026 under markedly different conditions compared to the frenzied demand cycles of recent years. Slower sales activity, moderated pricing, and higher borrowing costs have reshaped buyer behavior. For many investors, this shift raises an important question: does a softer market create risk — or opportunity?

Data from the Toronto Regional Real Estate Board (TRREB) indicates that overall GTA sales declined year-over-year entering 2026, while average prices experienced moderate softening in certain segments. At the same time, inventory levels have increased compared to peak conditions, creating more negotiation leverage for buyers.

Toronto Regional Real Estate Board (TRREB)

Against this backdrop, the condo segment — particularly apartment-style units — remains one of the most actively traded property types in the GTA. This article explores whether 2026 presents one of the strongest investment entry points in years for GTA condo buyers.

TRREB Market Watch and Home Transactions PDF

Understanding the Current GTA Condo Market

Condo apartments represent a significant share of total GTA housing transactions. Compared to detached homes, condos remain the most accessible entry point for both first-time buyers and investors. In recent market reports, average condo prices in many GTA subregions have adjusted downward compared to peak pricing levels.

This price moderation is significant for investors. When prices stabilize or soften while long-term population growth continues, potential upside improves over multi-year holding periods.

Statistics Canada continues to report strong population growth in the GTA, driven by immigration and interprovincial migration — both of which support rental demand.

Statistics Canada – Population Data

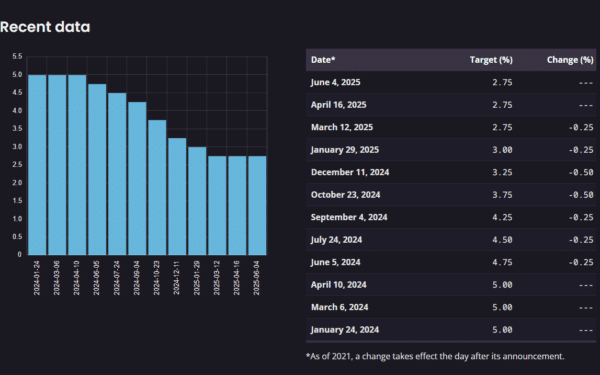

Interest Rates and Investor Psychology

The Bank of Canada’s monetary policy tightening cycle has influenced borrowing costs, affecting buyer confidence across all housing segments. Higher mortgage rates reduce affordability, which in turn cools short-term demand.

However, historically, periods of rate stabilization often precede renewed buyer activity. Investors who purchase during slower cycles sometimes benefit from:

- Greater price negotiation flexibility

- Reduced bidding competition

- More inventory options

- Longer decision windows

- Potential appreciation when rates ease

According to the Bank of Canada, interest rate policy is closely tied to inflation control, and future adjustments can significantly influence housing demand.

Bank of Canada

Rental Demand Remains Strong

One of the strongest arguments for condo investment in 2026 lies in rental fundamentals. The GTA continues to experience elevated rental demand, driven by immigration, student populations, and affordability constraints preventing some renters from purchasing.

The Canada Mortgage and Housing Corporation (CMHC) reports low rental vacancy rates across the GTA, which supports stable rental income potential.

Canada Mortgage and Housing Corporation (CMHC)

For investors, rental strength can offset short-term price volatility and provide cash flow stability during holding periods.

Condo Pricing Relative to Detached Homes

The affordability gap between detached homes and condo apartments in the GTA remains substantial. Detached homes often exceed the million-dollar threshold, while many condo units remain significantly below that level.

This affordability advantage means condos typically:

- Attract a broader buyer pool

- Offer lower capital entry requirements

- Provide stronger liquidity in resale markets

- Appeal to both end-users and investors

- Maintain demand during transitional markets

Liquidity is especially important for investors who may eventually reposition or rebalance portfolios.

Market Timing vs Long-Term Strategy

Attempting to perfectly time the bottom of a housing cycle is extremely difficult. Instead, many successful investors focus on long-term fundamentals: population growth, infrastructure development, employment centers, and transit expansion.

Major GTA infrastructure projects — including transit expansion and urban intensification plans — continue to support long-term condo demand, particularly near transit corridors.

Investors who evaluate properties based on location strength and rental fundamentals often prioritize strategic entry over short-term market noise.

Risks Investors Must Consider

While opportunities exist, investing in GTA condos in 2026 also requires realistic assessment of risks:

- Short-term price volatility

- Higher financing costs

- Condo maintenance fees

- Regulatory changes affecting rental markets

- Potential oversupply in certain submarkets

Conducting due diligence on building quality, reserve fund health, and neighbourhood supply conditions remains critical.

Who Benefits Most from Investing in 2026?

The current market environment may favor:

- Long-term investors with stable financing

- Buyers seeking rental income stability

- Portfolio diversifiers entering at moderated price points

- Investors targeting transit-oriented developments

- Cash buyers less affected by rate volatility

Short-term speculative investors may find the environment less predictable, while disciplined long-term investors may find strategic advantages.

Frequently Asked Questions

1. Are GTA condo prices falling in 2026?

Some submarkets have experienced price moderation compared to peak levels, while others have stabilized. Overall trends suggest more balanced conditions rather than dramatic declines.

2. Is rental demand strong enough to support condo investment?

Yes. Low vacancy rates and population growth continue to support rental demand in the GTA, which can help offset ownership costs for investors.

3. Should investors wait for interest rates to fall?

While rate reductions could stimulate renewed buyer demand, waiting carries the risk of increased competition. Strategic investors evaluate long-term fundamentals rather than attempting precise market timing.

4. What type of condo performs best as an investment?

Units located near transit, employment centers, and established amenities typically demonstrate stronger rental and resale performance over time.

5. Is 2026 the best time in years to invest?

For long-term investors seeking reduced competition and improved negotiation leverage, 2026 may present favorable conditions compared to peak-demand cycles. However, each investment decision should be based on individual financial strategy and risk tolerance.

Conclusion

The GTA condo market in 2026 reflects a shift toward balance rather than exuberance. While borrowing costs remain elevated compared to historic lows, moderated pricing, strong rental demand, and increased inventory provide investors with strategic opportunities. For those focused on long-term fundamentals rather than short-term speculation, this environment may represent one of the more favorable entry windows in recent years.

Disclaimer

This article is intended for informational purposes only and does not constitute financial, legal, or investment advice. Market conditions may change. Readers should consult qualified professionals before making investment decisions.