As living expenses rise, Canadians face a growing burden of debt that can be overwhelming. Household debt has become an increasingly serious issue for many people across the country. Owing to the high cost of higher education, many individuals have taken out significant student loans which, combined with their mortgage payments, add up to hefty household debt.

Facing a hefty sum of debt can take time and money to properly resolve, leaving you unable to save for certain things such as your dream home, car or retirement. Are you curious about the household debt statistics in Canada? Keep reading on to find out more!

2022 Updates:

- In April 2022, the Canadian household debt skyrocketed to an unbelievable US$2.116 trillion (according to CEIC Data).

- Recent statistical evidence reveals that in March 2022, the Canadian household debt percentage rose to an incredible 105.1% of Canada’s Nominal GDP (CEIC Data).

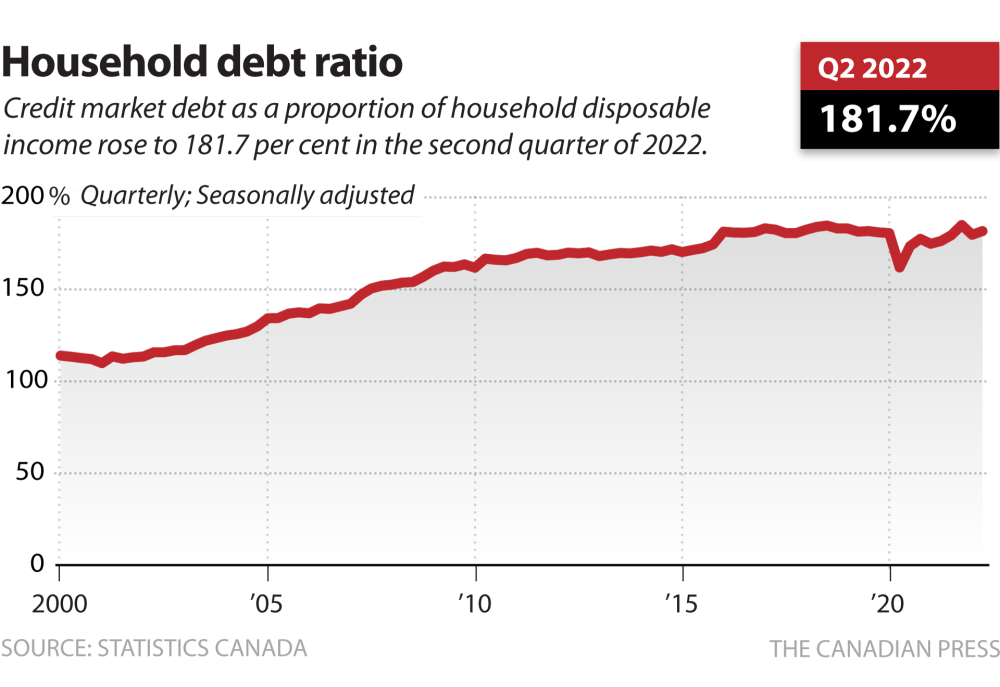

- In 2022, Canadian household debt hit an all-time high of 180.02% of the gross income – a worrying statistic reported by Trade Economics.

Canadians are Facing an Uphill Battle with Growing Household Debts

- The term “household debt” refers to the total amount of money owed by all members of a household.

- The typical Canadian household has an astonishing amount of debt – a staggering $41,500 – excluding mortgages.

- As of April 2022, Canadian households owed a total of $2.116 trillion in debt.

- In 2019, half of all Canadians earned an income less than the middle-ground median salary of $37,899.

- In 2021, mortgage borrowing saw an impressive 41% growth.

- In 2021, the debt-to-income ratio skyrocketed to 173.08%, a staggering 85% increase from the average rate of 88.77% in 1990.

- Canadians between the ages of 46-55 bear the greatest debt burden, with an average household debt (excluding mortgage) totaling a staggering $72,482.

- An overwhelming majority of Canadian households, nearly 60%, are currently in debt.

- Canadians typically have a credit score between 600 and 650, with scores higher than this range considered to be excellent.

- Startlingly, only 34% of Canadians are living debt-free and own their homes.

- In the 1960s and 1970s, household debt in Canada stayed below $200 billion; however, it has increased rapidly since then and currently stands at over $1 trillion.

- Struggling with unmanageable debt from loans and credit cards? Don’t worry. Talk to an expert today about consolidating your debts, and learn how you can save on expenses. Together we will create a plan that works for you!

What is household debt?

Before we focus on the household statistics for Canadians, it is important to understand what is meant by debt and how it differs from personal debt. It is often defined as the combined liabilities that require payments of interest or principal of all members in a household.

In other words, household debt is the combined amount owed by all members of a household.

Types of debt

There are different types of debt that contribute to household debt, which include:

- Secured debt, which is any type of debt that is backed by collateral. This collateral will be forfeited to the lender if the debt is not paid. The amount you are able to borrow is determined by the value of the asset used as a collateral. An example of secure debt would be a car loan where the lender will repossess the car if the loan isn’t paid.

- Unsecured debt is not backed by collateral and includes debt from credit cards and unsecured loans. How much you can borrow is based on your credit score. The better your score, the more you can borrow.

- Mortgage debt is a subset of secured debt where the property is the collateral. Most people will pay back their mortgage over several decades.

- Student loans can be government issued or private loans. They are a type of unsecured loans as there is no collateral used.

The average household debt in Canada

Without factoring in mortgage debt, the typical indebted individual owes a staggering $20,739; thus making two-person households liable for nearly $41,500 collectively. Nevertheless, when mortgages are added to this assessment of average per person debt in Canada – that number skyrockets up to an unparalleled amount of almost seventy five thousand dollars!

Canadian households had amassed a staggering $2,116 billion in debt by April of 2022- although this number is lower than the amount which was reported for 2020: $2,330 billion. Mortgages accounted for the most considerable portion of household debt at an impressive total of $1,550 billion with non-mortgage loans and consumer credit making up the difference of roughly $802 billion. (Source)

The average earnings and net worth of Canadian households

In 2019, the median annual income in Canada was $37,899 according to Statistics Canada – not the average yearly salary of $49,000. This is an important distinction; 50% of Canadians earned less than this amount.

Outliers can deceive an individual’s understanding of the average income, which is why median statistics are often more useful when studying data on salaries.

According to Statistics Canada, the net worth of Canadians increased by a striking 3.5% annually between 2012 and 2016. Fast-forwarding to 2019, their median net worth amounted to an impressive $329,000!

Boasting a millionaire population of near one million, the median net worth gives us an accurate reflection of Canada’s wealth distribution. Toronto and Vancouver have the highest median net worth while Montreal has the lowest – Calgary, Edmonton, and Ottawa fall somewhere in between.

What is the primary factor that has caused households to become more and more indebted?

This year, Canadian households are bearing a heavy burden of debt- largely due to the rapid surge in mortgages. It’s no wonder that new mortgage borrowing skyrocketed by an astounding 41%, pushing household debt levels higher than ever before.

Despite this, non-mortgage debt decreased as government issued funds helped many Canadians to pay off their credit card bills. Plus, the lockdowns caused households to spend less money altogether.

Who is most likely to be encumbered with the greatest debt?

Data reveals that Canadians in the 46-55 age bracket owe the greatest amounts of money. Without mortgages, their consumer debt averages around $36,241 while total household debt stands at an estimated figure of $72,482.

Young Canadians, aged 18-25 were in debt to the tune of $8,847 on average at the start of 2020. As those ages increased so did their obligation: 26-35 year olds had an outstanding balance of $18,398; 36-45 owed around $28,863; 56-65 inked a hefty sum totaling up to a staggering amount – approximately 30K! Surprisingly enough though seniors over 65 held a modest estimated total liability at just under 17 grand ($16,491).

What percentage of Canadian households are financially independent and free from debt?

According to Statistics Canada, only 3 in 10 Canadians are debt-free – a figure rising to almost 6 out of 10 for households headed by those aged 65 or over. The growth in seniors’ indebtedness is largely attributed to an increase of mortgage borrowing and credit card use throughout the past few decades.

Mortgage statistics

Lending for mortgages has skyrocketed in 2021, with a surge of 41% compared to the year before. But what other mortgage-related figures exist across Canada? In 2020 alone, Canadians had borrowed an astounding $1.7 trillion on their mortgages – marking the most substantial climb since 2010 when this debt increased by an impressive $118 billion within one single year! Low interest rates and rising property values were instrumental contributors that propelled such spending growth in this sector. This potential hazard is reminiscent of the 2008/2009 financial crisis, when soaring mortgage rates pushed many people into purchasing properties beyond their means. This could be a perilous situation if history repeats itself.

Astonishingly, only 34% of Canadian households own their homes outright. Not surprisingly, these homeowners are more likely to be debt-free and possess fewer liabilities than those with mortgages. This data reveals the breadth of home ownership across Canada; it is clear that for most Canadians mortgaged houses are a reality rather than an exception!

What is the standard credit rating among Canadians?

Equifax Canada has determined that the average Canadian credit score lies between 600 and 650. Credit scores are calculated based on multiple factors such as payment history, debt levels, and length of credit. Canadians who possess a score of 650 or more show financial stability making them likely candidates for loans from lenders. An excellent credit score is one above 760 points according to Equifax’s research findings.

Uncovering Canada’s history of household debt – from its beginnings to today.

Every year in Canada, the total household debt has increased since 1961 when records began. In the 1960s and 1970s, even though there was growth each year, it was slow and consistent. The total debt remained below $263 billion. However, by the end of the 1980s decade, the debt had risen to over $500 billion and surpassed 1 trillion in early 2000.

Over the years, family debt has gone through an array of transformations.

Over the past several years, household debt in Canada has undergone dramatic shifts- particularly when examining the ratio of total debt to household income. In the 1980s, this figure was 66%, yet now it stands at 173.08%. Clearly, Canadian households owe much more money than they did thirty years ago – and a major factor is that most people cannot purchase their home without taking out mortgages. Undoubtedly, these numbers are concerning but also serve as an important reminder of how essential financial literacy and responsibility can be!

Despite Canadians earning more than they ever did before, the debt to income ratio still stands at $1.73 for each dollar earned – a clear indication that what’s left in their pockets is less than what they owe. This unfortunate statistic can be traced back to 1961 when the total amount of Canadian household debt was merely 16 billion dollars; now it’s over 2 trillion!

Nevertheless, there is an optimistic side to this story. The proportion of debt from credit cards has been on a downward trajectory in Canada and recently reached a six-year low. This decrease is closely correlated with the restricted spending due to COVID-19 restrictions. Furthermore, the overall debt to income ratio was higher prior to the pandemic – it was estimated at 180% during Q4 2019! In short: Canadians have made strides towards reducing their reliance on borrowing money which can only lead us down a path of financial wellbeing going forward.

What factors have contributed to the sharp rise of household debt in Canada since the mid-1900s?

As the economy flourished after WWII, Canadians took on more debt with a newfound attitude towards it; instead of viewing debt as something to stay away from, people began embracing taking out loans and using credit. This shift in perspective marked an increase in debts throughout Canada.

Following WWII, Canadians’ access to loans and the use of credit grew in popularity. Though spending on credit became more accepted, it wasn’t until the 1990s that household debt skyrocketed throughout Canada.

Since its foundation in 1971, the credit score system has been improved to make it simpler for those earning a median wage to obtain loans.

Are you concerned about the impact of debt on your financial future? If so, there are several concrete steps that you can take to manage and reduce this burden.

Struggling to stay on top of debt payments? You’re not alone and there are resources available to help. Start by utilizing a debt calculator – an effective tool that will estimate your repayment timeline as well as the amount of interest you’ll end up paying. Knowing this information is essential for establishing a successful plan towards becoming financially free.

Utilizing a debt calculator can give you an indication of whether or not you are capable of taking care of the debt yourself by allocating extra cash each month to increase payment speed. If your budget only allows for minimum payments, or even worse if it is unable to cover them in full, consulting with a financial professional may be beneficial as they can assist in minimizing expenses through methods such as consolidating loans and decreasing outgoings.

Conclusion

Despite the vast amount of household debt in Canada, it is not necessarily an indication that a financial crisis will arise. While there are common elements to past recessions including historically low interest rates and booming real estate market conditions, banks have been more mindful of lending large amounts to unstable households with poor credit ratings.

As people spent less during the lockdowns following the pandemic, the ratio of debt to income in Canada slightly improved. However, it is still too soon to tell what has happened since the return to a more normal life.